Being back in India for a decade now, after having spent years working in the US, I am often approached by non-resident Indians (NRIs) keen to invest in this country’s growth. Many enquire specifically about the booming real estate sector. Below are the most common questions I hear.

Why should I buy Indian property when I have so many other options?

This is a sensitive question. Those who end up buying give me all kinds of reasons, such as “I will always be an Indian at heart,” “Knowing that I have a place back home gives me comfort,” and “Prices are shooting up and I want to lock it in.”

Those who don’t buy give me even more interesting answers: “It’s too much hassle,” “I would rather invest in the stock market,” “I have a friend who got ripped off,” or “I don’t know if I can get my money back in dollars and don’t want to be stuck with rupees.”

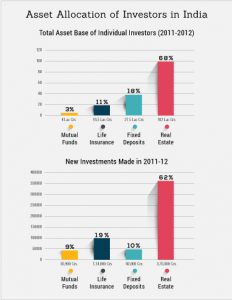

There is truth in all of these sentiments. Emotional reasons are hard to pin down, so I won’t try. But if you do not invest at all in Indian real estate, you risk missing a profound opportunity to grow your wealth. Indian real estate today is arguably one of the world’s foremost investment opportunities, as the country’s economy is in the midst of the strongest development in its history. This exciting asset class can give predictable annualized returns (IRRs) in excess of 20 percent—and that too in a tangible asset that you can literally step into!

There is truth in all of these sentiments. Emotional reasons are hard to pin down, so I won’t try. But if you do not invest at all in Indian real estate, you risk missing a profound opportunity to grow your wealth. Indian real estate today is arguably one of the world’s foremost investment opportunities, as the country’s economy is in the midst of the strongest development in its history. This exciting asset class can give predictable annualized returns (IRRs) in excess of 20 percent—and that too in a tangible asset that you can literally step into!

However, this is a terrific investment only if you avoid some of the pitfalls unique to this country. Before parting with your hard-earned money, you should first become familiar with the matters described below.

Are NRIs allowed to invest in Indian real estate?

The short answer is yes. An NRI—defined as an Indian passport holder living abroad or a foreign citizen who (a) was at one time a citizen of India or (b) is the child or grandchild of a citizen of India—can purchase most types of property in India. Although the only proof of NRI status required at the time of purchase is an affidavit, an NRI will need documentary evidence at the time of resale and repatriation of funds. These include:

- An Indian passport, an Overseas Citizen of India card, or a Person of Indian Origin card

- PAN card (This is an Indian tax account card which is very easy to obtain. Most professional organizations you would invest through can arrange one for you.)

What types of properties am I allowed to buy?

NRIs may purchase residential, commercial, and industrial properties in India. NRIs are not permitted to purchase agricultural properties or plantations, although they can own such by way of gift or inheritance.

Which property types make the best investments?

Although every property type has its advantages, some of them are more suitable for NRIs than others. Below are some general considerations.

Commercial Real Estate – Commercial real estate is preferred by investors who are ready to deploy larger amounts of capital and are more focused on cash flows than appreciation. Commercial properties generally give an approximate cash yield of around eight percent after expenses and a typical annual appreciation of five percent,  for a total return of around 13 percent before taxes. Selecting commercial properties requires some expertise because many older properties—and even some new ones—do not meet the needs of modern tenants.

for a total return of around 13 percent before taxes. Selecting commercial properties requires some expertise because many older properties—and even some new ones—do not meet the needs of modern tenants.

Industrial Property – Industrial properties are similar to commercial properties but require a greater degree of expertise, as the vacancy rates on a poorly selected property can be quite high.

Residential Land – Land usually gives the highest overall returns if the title is good and the location has been vetted properly. The best land investments tend to be parcels in residentially zoned areas where home prices are increasing rapidly. Future prices are of course difficult to predict, but recent trends suggest that a land investor can expect annual returns of approximately 25 percent and can double his money every three to four years. Since land does not generate any cash flow until it is resold, it is most suitable for aggressive investors who are focused on maximizing returns as opposed to generating income. Land can be purchased either directly from an owner or as part of a gated community, which in India is sometimes called a layout or plotted development. For NRIs interested in purchasing land, I recommend doing so in a development to minimize risks such as a title defect or encroachment. Buying from a developer also ensures that you can pay through normal banking channels; by contrast, many individual sellers expect a significant part of the sale price in cash.

Apartments – Flats are attractive because they promise strong returns (around 18 to 20 percent annualized if purchased below market price) and the potential to earn cash flow from renting them out. To earn predictable returns in an apartment, it is important to buy it before launch and at a substantial discount to the launch price. The discount will depend on how much of the purchase price you are willing to pay up front. In addition, you can often get a better deal if you go through an aggregator rather than trying to negotiate individually with a developer. It is important to select a city that has stable and affordable prices and a high population growth rate. Some of the Tier 1 cities that I like are Bangalore and Pune, and some of my favorite Tier 2 cities are Ahmedabad and Vadodara (Baroda).

Villas – Villas, or single-family houses, have investment characteristics similar to apartments but with a somewhat higher appreciation rate because they have a larger area of land per square foot of built-up area. Villas can yield returns somewhere between that of apartments and land. Their selection criteria should be similar to that of apartments – buy early at a discount and in the right location.

Should I buy pre-launch or post completion?

Investors who are primarily concerned with cash flow tend to purchase properties that are already constructed. But this can be a costly mistake. Any real estate development has two distinct phases: (a) the development phase when raw land is being transformed into something much more valuable such as an apartment building, and (b) the occupancy phase, where much of the value addition has already occurred and growth will depend on inflation.

During the development phase, values tend to grow rapidly because developers increase prices every month or quarter depending on sales velocity. The best deals are often available to an exclusive club of investors before the official launch of the project. NRI investors will do well to get on these pre-launch offering lists or to use an aggregation service that brings to them deeply discounted pre-launch deals.

Where in India should I buy?

People throughout the world tend to invest in their own cities and neighborhoods. NRIs are no exception, and most investments by NRIs flow back to the cities and states of their origin. While this is understandable, India’s highly uneven growth makes this a risky financial move. Cities which were considered growth destinations a few decades ago, such as Mumbai (Bombay) and Kolkata (Calcutta), are today slow-growing mature markets with limited potential. Young, fast-growing cities such as Bangalore and Pune offer an enviable combination of rapid growth, low current prices, and a high percentage of population working in the well-paid tech sector. It is these cities and some fast-growing Tier-2 locations that will give the best returns. Modern India is not what it was 10 years ago, not even what it was five years ago. Today, it is easy to purchase and resell property remotely using ethical and professional firms that can provide you with efficient property services in cities of interest to you.

Should I buy resale properties and generate rental income?

Generally, this is a bad idea. Why? Unless you’re getting an amazing deal or a distress sale, the price is going to be at the market rate or even higher. Residential rental yields in India are among the lowest in the world, ranging from two to four percent before expenses and maintenance. Therefore, nearly your entire investment return is going to come from speculative future appreciation. You will generally be better off buying new properties at a significant discount to the market so that much of your profit is locked in at the time of purchase. You can think of price appreciation as icing on the cake. And you can avoid the hassle of managing a tenant who may be picky or worse, not pay rent on time.

How do I pay for the property?

RBI regulations have been relaxed over the years, and prior permission is not required for an NRI to buy real estate in India. The rules for any such property transaction fall under the Foreign Exchange Management Act. Transactions must take place through normal banking channels and in Indian rupees. You may pay for the purchase by wiring money from abroad, sending your foreign check to India, or by paying from an account that you hold in an Indian bank.

How do I get my money back in dollars or other hard currency?

NRIs are permitted to repatriate up to USD 1 million per year from their accounts held with Indian banks. Non-Resident Ordinary Rupee (NRO) accounts are easy to set up; most professional real estate service firms will assist you in establishing one. NRIs who wish to repatriate in excess of USD 1 million per year will need to find alternate ways to enter the Indian real estate market so as not to be limited by the dollar restriction.

I don’t want to lock in my money for five or seven years while waiting for the flat. Will I lose money if I want to sell before a project is complete?

This is one area in which there has recently been a big change. Previously, the only way you could invest in India was to lock your money into one specific project for multiple years. Today, there are options which enable you to buy now, exit within a couple of years, and take your profit out. (Full disclosure: My experience in this comes from SmartOwner, a real estate company run by friends of mine.)

Do I have to pay taxes both in India and my current country of residence?

Chances are that the answer for you is no. India has double taxation avoidance agreements with more than 80 countries. When you buy, there are no taxes to pay. When you sell, taxes will be deducted in India before you get your money wired to your country of residence. Most people will be able to offset the Indian tax against any tax payable in their country of residence.

How do I generate good returns?

We all know that real-estate prices will go up in the long run, but if you are like me, you want both short and long-term gain! How does one achieve that? As the old saying goes, the three most important factors in real estate are location, location, and location. However, in India, there are several other important considerations (Read about the 10 criteria to use when selecting real estate in India).

Here, I will focus only on the main lessons that I have learned: what type of property to buy and when to buy it. In my experience, new residential properties (plots, apartments, and villas) are the top investment options. The ideal time to buy is very early in the launch cycle, and the way to do so is from a service provider who is able to negotiate bulk discounts from developers. If you buy with a steep enough discount, you will have locked in a sufficiently high profit at the time of your purchase that your investment can do quite well even if prices appreciate less than expected.

For the savvy NRI, now is a great time to buy real estate in India—a country that is poised to be one of the best investment destinations the world has seen. Those of Indian origin are uniquely placed to take advantage of this fantastic opportunity.